The idea of retiring in your 50’s as opposed to your 60’s appeals to many Americans, and for good reason. Why postpone the good life, right? However, if you are serious about retiring early, you need to plan in advance and make sacrifices many years ahead of time.

Here are 8 areas to consider if your serious about retiring in your 50’s:

1. Free Time

Many folks welcome any free time they can get, yet don’t consider how to manage it once they retire. It’s important not to dismiss the notion of being bored in retirement. Think about your social circle (spouse, friends, colleagues, etc.) who may still be in the workforce. Your schedules could potentially look very different once you retire, leaving you with a lot of free time you may not be used to.

Before retiring, think about things you’d like to do on your own – volunteer in the community, hike local trails, try a new workout class, etc. Ideally these new activities won’t cost you a lot of money, and might even give you the chance to earn some “fun money”. Consider the costs involved with how you spend your new free time, but most importantly, make sure these new activities give you purpose when you wake up in the morning. This is your chance to get creative, so have fun with it!

2. Debt

Becoming debt free should be a priority at any stage in life, especially if you want to retire in your 50’s. If you’re aiming to retire early, rid yourself of any consumer debt like credit cards and auto loans. Of course, paying off your mortgage is a major plus, but it may not be realistic for everyone. Regardless if you own or rent, prioritize keeping your housing related expenses manageable that way you increase your cash flow. By eliminating debt service payments (expense), you will fund your retirement accounts (income). If you’re serious about retiring in your 50’s, get aggressive about eliminating consumer debt.

3. Expenses

Retirement expenses are directly tied to your debt and how you spend your time. As you begin to plan for retirement, it’s important to be transparent when it comes to your expenses. All too often people don’t take an honest account of how much discretionary spending they do – eating out, entertainment, travel, etc. – and it throws off their projected retirement expenses.

You can safely expect to spend an extra 10% – 15% over your planned budget for the first couple years of retirement. This gets you ahead of the game and provides a buffer if you need it. The last thing you want to do is retire, only to come to the realization that you’ve significantly miscalculated your discretionary budget. It’s better to be upfront and honest about your spending habits before retirement than have to adjust later once you’re retired.

4. Cash Reserves

The need for adequate cash reserves is never more important then it is in retirement. Life is always throwing curve balls our way and that does not change in retirement. In my experience, the better you prepare, the less likely emergencies strike. Beef up your cash position and plan for any large purchases. A general rule of thumb is 3 to 6 months of expenses, but in retirement I would certainly lean toward 6 months.

If you have trouble saving up your emergency fund, consider setting up an allotment from your paycheck to a bank separate from where you have your primary checking account. Out of sight out of mind. Last minute weekend getaway or new patio furniture: not an emergency. Roof fails or air conditioning unit dies in July: emergency.

5. Retirement Savings

Most Americans have a large portion of their money in retirement accounts – 401(k)s, IRAs, 403(b)s, TSPs, 457, etc. These accounts are ideal for retirement savings due to tax benefits. However, keep in mind most employer-sponsored retirement plans have early withdrawal penalties prior to age 55. IRAs and Roth IRAs have penalties for withdrawals prior to age 59.5.

As you approach retirement, do your research on different retirement account options. There’s a 72(t) early withdrawal provision that allows substantially equal periodic payments from a retirement account as long as the distributions last until age 59.5 or 5 years, whichever is longer. You can also fund a non-retirement brokerage account early and often. These types of accounts allow you to investment in the same way you can in retirement accounts without early withdrawal penalties. Explore the pros and cons of each, it’s best to know all your options.

6. Social Security

The earliest you can start collecting Social Security is age 62, so there’s really no need to factor it in. However, if you are planning on earning income in retirement, you’ll want to be aware of the social security earnings test. In 2018, Social Security will withhold $1 in benefits for every $2 of earnings in excess of $17,040. This applies in years before the year of attaining NRA (Normal Retirement Age).

If you are in your 30’s or early 40’s, you may not want to factor Social Security income into your retirement plan at all. Not because you won’t receive Social Security (although a lot can change in 15-25 years), but it’s always better to be over-prepared than under-prepared.

7. Withdrawal Rates

If you’re planning to take income from your investment portfolio when you retire, you’ll want to be sure you’re taking it at a sustainable withdrawal rate. The money will need to last you 30, possibly 40+ years. If you are starting income distributions from your investment portfolio in your 50’s, you’ll want to avoid anything higher than a 3% – 4% withdrawal. Play around with the numbers to make sure your withdrawal rate is sustainable for retiring in your 50’s. The last thing you want to do is outlive your money.

8. Health Insurance

Medicare starts at age 65, so if your employer does not offer you the ability to continue health benefits into retirement, you’ll need to factor in the cost of increased health care costs between retirement and age 65. Do your research and plan on the costs increasing between now and retirement. If you have a spouse and they have coverage through their employer, consider switching to their policy.

Be sure to periodically reassess your goals. You may have set a goal years ago that has lost its luster today. If you always had the goal of retiring in your 50’s, for example, but find fulfillment in your work, don’t hold yourself to a goal you made years ago. I’ve seen folks retire because they’ve romanticized the idea of retirement for so long, only to end up regretting the decision. It’s okay if your goals change, just make sure they align with the season of life you’re in.

Retiring in your 50’s is absolutely doable, but requires planning and smart changes to your personal finances now. As a part of the workforce, you’re trading your time for money. However, once you retire, this is no longer necessary to meet your lifestyle. That doesn’t mean you shouldn’t work or do income-producing activities. In fact, if you can have fun, meet new people, or follow a passion while generating income, that’s an added bonus. However, if after running the numbers you know you’ll have to work in retirement, take a step back and reevaluate your situation. It might be a good idea to get an unbiased opinion from a financial planner to look at your situation.

If you’d like to discuss your options with us, book a call using this link and we’ll be in contact with you shortly.

For federal employees approaching retirement, there are a lot of questions and considerations to take into account. One of the more well-known and frequently asked questions involves the Thrift Savings Plan (TSP), specifically whether you should leave your retirement savings in the TSP or move them to an IRA.

It’s a weighted question and one that often causes confusion with all the varying opinions and biased information out there. In an effort to simplify, let’s compare the TSP vs. IRA by solely focusing on the costs, since that’s what most folks are concerned with anyways.

Breakdown of Expenses

There are three major areas to prioritize when deciding what to do with your TSP in retirement:

- Investment options

- Liquidity (access to your money)

- Cost (expenses associated with the investment vehicle and underlying investments)

The challenge with comparing TSP to IRA expenses is that most of the information found online is simply inaccurate. Generally, the assumption is made that there will be high expense investments in the IRA or an investment professional will be hired to manage the IRA. This is not a fair comparison because the additional investment options or investment advisory services are not being offered within the TSP. Conversely, high expense investments and hiring an investment advisor to manage your IRA is not mandatory, so it’s not an “apples to apples” comparison.

A more accurate comparison would look at managing your own IRA using low cost index funds. Outside of the G Fund, the objective of all the other individual funds (C, S, I, F) is to match the performance of broad indexes.

- F Fund – Objective is to match performance of the Bloomberg Barclays U.S. Aggregate Bond Index

- C Fund – Objective is to match performance of the Standard & Poor’s 500 Stock Index

- S Fund – Objective is to match performance of the Dow Jones U.S. Completion Total Stock Market (TSM) Index

- I Fund – Objective is to match performance of the MSCI EAFE (Europe, Australasia, Far East) Index

- G Fund – Invested in short-term U.S. Treasury securities specifically issued to the TSP, and rates are similar to U.S. government bonds and notes

So why can’t you do that on your own outside of the TSP? Well, you can.

Investment Expenses

If the TSP Funds simply track broad index performance, then the question becomes what is the most cost efficient way to do this in an IRA? Many low cost mutual funds and Exchange Traded Funds (ETFs) track the performance of broad indexes in the same way the TSP funds do. ETFs also have expense ratios very close to that of the TSP’s expenses and in some cases, slightly lower.

One example is the SPDR Portfolio Total Market (SPTM) Stock Market ETF and SPDR Portfolio Large Cap ETF Index (SPLG). Both have net expense ratios of .03% and the TSP’s net expense ratio is .033% as of 2017. If you’re looking at fixed income / bond funds, the SPDR Portfolio Aggregate Bond (SPAB) ETF has a net expense ratio of .04%. As for the G Fund, there are Short Term Treasury mutual funds and ETFs with expenses comparable to the G Fund. You can also consider purchasing individual Treasury bills and notes, which do not have an expense.

Are There Hidden Fees?

The .033% TSP expense is all inclusive. There are no additional annual maintenance fees or trading costs, however; interfund transfers are limited in the TSP. Every financial institution is different when it comes to annual maintenance fees and trading costs with IRAs. If you do your research, you will find that many of the large firms have no annual maintenance fees and a robust list of No Transaction Fee (NTF) Mutual Funds and ETFs.

In a Nutshell

If you are eager to keep costs low and manage your own retirement account, you can nearly recreate the investments options and low expenses of the TSP in your own IRA. Certainly there are many other options available if you chose to move to an IRA from the TSP that could have increased costs. As with all things, there are pros and cons.

Many people rely on guidance of an investment professional / financial advisor to help them manage their investments and financial goals. Vanguard conducted an insightful study stating that an advisor may add up to 3% in net portfolio returns over time. However, if you are an investment “DIYer”, then don’t listen to the hype about high IRA fees. Is an IRA more expensive than the TSP? In short, no. Can an IRA be more expensive than the TSP? Yes, but that is completely up to you.

If you’d like to discuss your options with a federal retirement advisor, book a call using this link and we’ll be in contact with you shortly.

Past performance doesn’t guarantee future results.

It’s no secret that college expenses add up quickly. Nowadays, paying for college takes time and careful consideration of a family’s finances. Good news is there are plenty of saving plans available to help pay for college – the most popular one being the 529 Plan. The biggest appeal of the 529 Plan is it offers tax free growth when used to fund qualified higher education and high annual contribution limits. However, there are a few scenarios (one in particular) where a Traditional or Roth IRA may be a viable option to consider.

The most common scenario occurs when there hasn’t been any money set aside for your child approaching college – not in the budget, simply overlooked, unsure of a college savings account benefits, or any number of other reasons – but you have an IRA or Roth IRA account and you feel it’s important to help your child pay for their college education.

In this case, there is an exception that allows IRA distributions for qualified higher education expenses like tuition, books, supplies, fees and room and board, etc. as long as the student is enrolled in a degree program. This exception allows you to avoid the 10% early withdrawal penalty on IRA distributions if you are under the age of 59.5. If you are older than 59.5, this exception does not apply to you as there no penalties to withdraw from your IRAs at that age.

Balances in IRAs and Roth IRAs are not used for financial aid need analysis purposes and should not affect financial aid eligibility. However, withdrawals from IRAs are generally treated as income and may affect eligibility. Even withdrawals from Roth IRAs are treated as untaxed income and may affect needs based financial aid eligibility the year following the withdrawal.

So basically you have a traditional IRA being used as a tax-deferred college savings vehicle. If you are able to limit your withdrawals from a Roth IRA to contributions only, the distribution is not only tax free, but penalty free as well when used for qualified higher education expenses.

I want to emphasize that prior to considering this option, it is absolutely imperative you thoroughly review your finances to make sure this will not put your financial future and retirement plans at risk. I’m not an advocate of borrowing or withdrawing from retirement accounts for any reason outside of providing for life in retirement, and I strongly advise against placing your financial future in jeopardy to fund your child’s college education. I have seen this happen far too often with very poor outcomes – becoming a financial burden to the kids later on, pushing back retirement or worse, not being able to retire at all. I have also seen folks withdraw significant portions of their IRAs to fund their kid’s college, only to see them drop out.

To be clear, I am not suggesting student loans. However, the fact is students can borrow money for college and there are no retirement loans available, as far as I know. If your child needs to take out a loan, by all means consider helping them pay off their student loans once completing their education. Whatever you decide to do, make sure you prioritize evaluating the long term effects this will have not only on your finances, but theirs as well.

Other important considerations include:

- Distribution and expenses must happen in the same years

- Qualified educational expenses can only be used towards one educational tax benefit (no double dipping!) Ex: you can’t take a penalty-free IRA withdrawal and use the same expense toward a Lifetime learning tax credit.

- You can’t replenish the funds you withdrew from your IRA account except by normal annual contributions, which are subject to annual limits

If you’d like to discuss your options, book a call using this link and we’ll be in contact with you shortly.

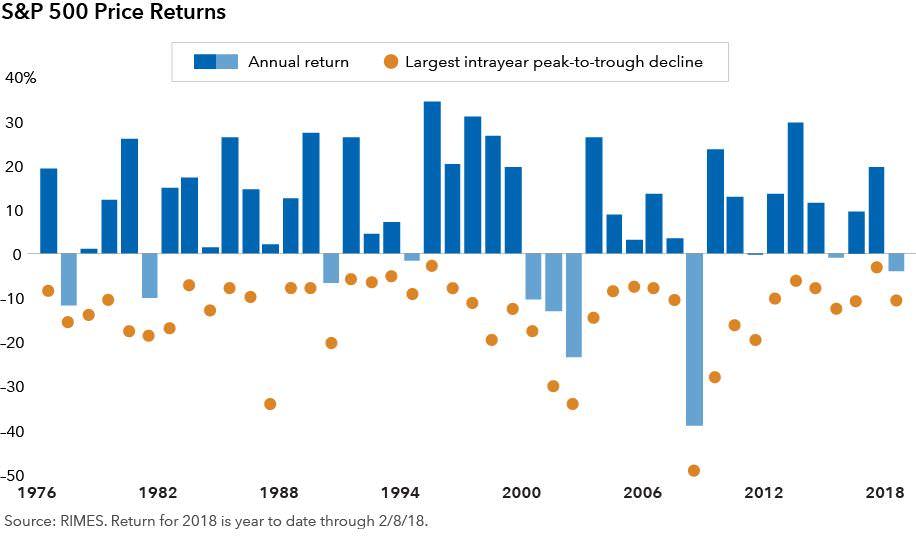

By all accounts it has been a phenomenal run for stocks. Through the end of 2017, the S&P 500 has had a positive total return in 19 of the last 20 quarters. The S&P 500 recorded a loss of 0.8% in the first quarter of 2018. This is the ninth time since 1990 that the stock market was negative during the first three months of the year. The S&P 500 went on to record a positive return for the entire year in five of the previous eight years that started with a loss (1992, 1994, 2003, 2005 and 2009) and suffered full-year of losses in the other three years (1990, 2001 and 2008).

It’s also clear that market volatility is back in 2018 versus the remarkably low volatility we experienced in 2017. To put things into perspective, the S&P 500 in 2017 had a total of nine 1% gain or loss trading days. In the first quarter of 2018 alone, the S&P 500 has had more than 20 1% gain or loss trading days. Given the uptick in volatility and panic inducing, sensationalized media coverage, I would like to provide you with three tips to help you stay focused on your long term goals and avoid undue stress that can accompany short term declines in the market.

1. Tune out the news and don’t act on emotion

In case you didn’t know, the news media outlets may not have your financial interest in mind. Their goal sometimes is to keep you in fear and tuned in for better ratings. Market pull backs are normal and should be expected in exchange for the opportunity of achieving long term growth.

As demonstrated by Nobel Prize-winning psychologist, Daniel Kahneman, loss-aversion theory says that people feel the pain of losing money more than they enjoy gains. Naturally, investors flee the market during sudden, sharp declines and in the same way, greed motivates them to jump back in when stocks are on the rise. Both of these natural impulses can be devastating to your long term goals, but investments rooted in proper education, unbiased research and proven strategies can overcome the impulse and pull of emotion.

Below is a chart showing intra-year declines (orange dot) of the S&P 500 as well as annual year end returns (blue bar):

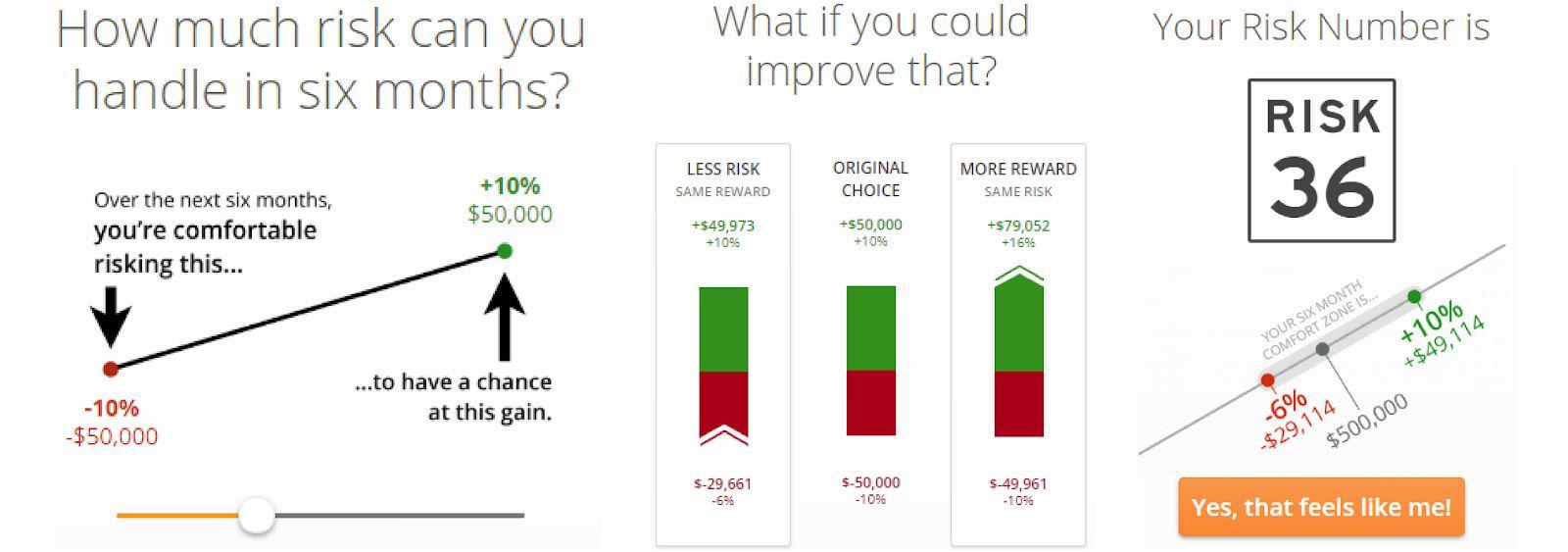

2. Change your investments proactively, not during market declines

Riskalyze Services are for informational purposes only and do not constitute investment advice or an investment recommendation.

Ideally, you have taken the time to properly assess your risk tolerance and aligned your investments (as shown above) with your ability to endure volatility. If done properly, the ups and downs in your portfolio shouldn’t cause you to have a knee jerk reaction at inopportune times. I recommend stress testing your portfolio to see how it may have performed in both good and bad years.

Below is an example of a stress test:

Riskalyze Services are for informational purposes only and do not constitute investment advice or an investment recommendation.

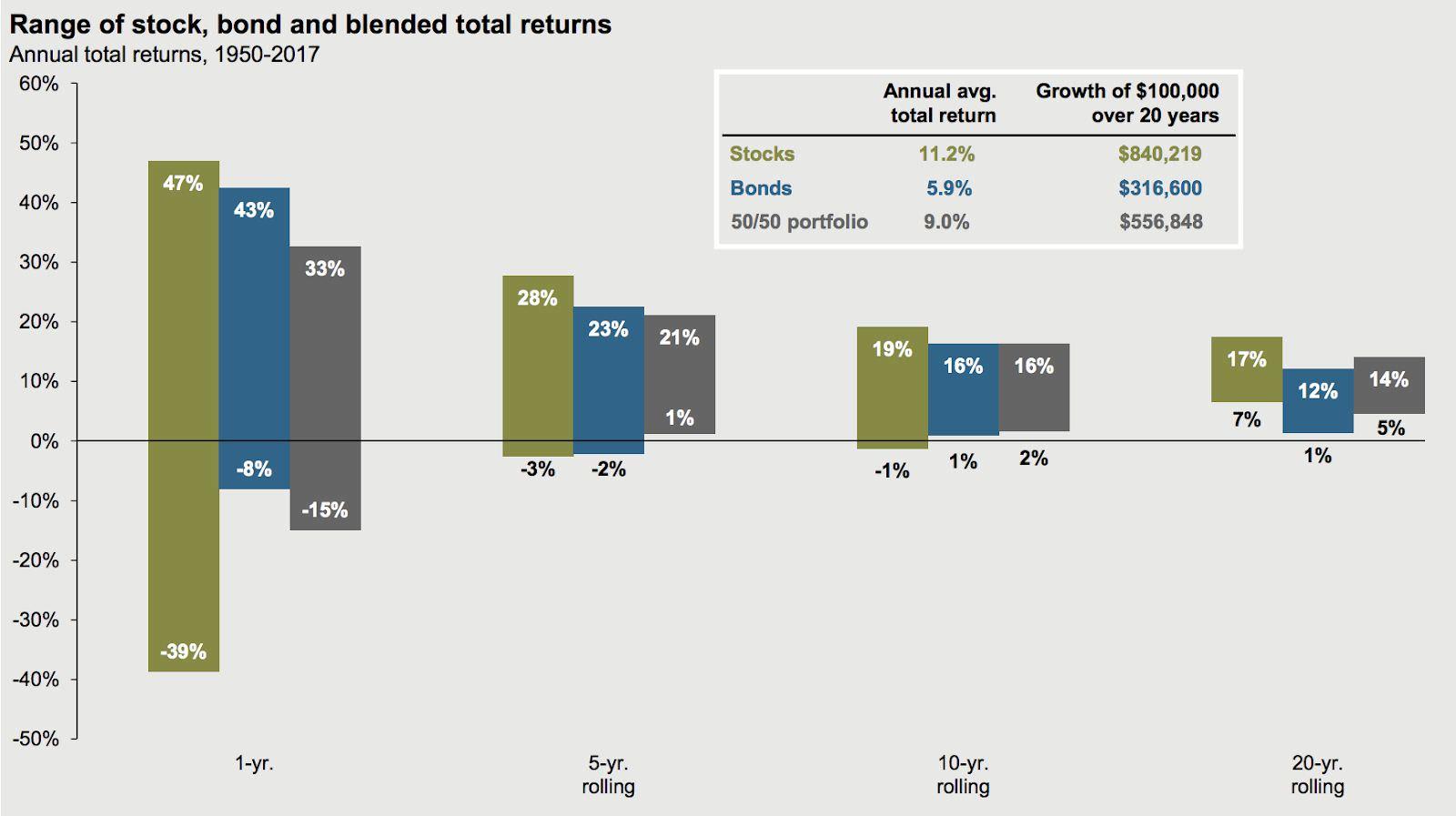

3. Be patient, your investments may thank you later

It is almost impossible for anyone to accurately predict short-term market moves, and investors who sit on the sidelines risk losing out on periods of meaningful price appreciation that may follow sharp market downturns. The visual below shows how allowing emotion and impatience to dictate your investment decisions can affect your long-term financial goals.

Many let emotion get the best of them during the 2008 and 2009 market downturn causing them to sell investments in their retirement accounts resulting in significant losses. Moreover, many did not reinvest for several years and missed out on several high growth years that followed.

This chart clearly illustrates how patience pays. One year losses are common, however; a blend of stocks and bonds have not suffered a negative return in any five-year rolling period. This information does not imply that all future five-year rolling periods will mirror the past. However, understanding historical market data is a powerful tool to “fight the fear” that market volatility can bring about. Past performance does not guarantee future results.

Source: Barclays, Bloomberg, FactSet, Federal Reserve, Robert Shiller, Strategas/Ibbotson, J.P. Morgan Asset Management. Returns shown are based on calendar year returns from 1950 to 2017. Stocks represent the S&P 500 Shiller Composite and Bonds represent Strategas/Ibbotson for periods from 1950 to 2010 and Bloomberg Barclays Aggregate thereafter. Growth of $100,000 is based on annual average total returns from 1950 to 2017. Guide to the Markets – U.S. Data are as of March 31, 2018. Past performance doesn’t guarantee future results. Examples are for illustrative purposes only. Riskalyze Services are for informational purposes only and do not constitute investment advice or an investment recommendation. Riskalyze Services are for informational purposes only and do not constitute investment advice or an investment recommendation.

The Overview

The U.S. Senate recently passed a new tax bill titled, “Tax Cuts and Job Act”. President Donald Trump signed this bill, stating that it will be beneficial both to individuals and corporations. The bill will go into effect for 2018 taxes, bypassing 2017 taxes.

The Breakdown

The bill has a wide range effect, impacting all taxpayers to a varying degree. As always, your income will significantly impact your taxes – those in higher tax brackets will feel a bigger impact. However, there are many tax brackets that are lowering.

Analysts have noted that the standard deduction will nearly double for many households, which means many will opt to take that rather than itemize their taxes in the coming years. In addition, the child tax credit for each child under the age of 17 has significantly increased from $1,000 to $1,600 per child. It’s also important to note that the personal tax exemption has been eliminated under this new tax bill, which could be a setback for some households.

The Implications

If you’re anything like me, hearing the news of a new Senate Tax Bill brought one question to mind, “What does this mean for me, specifically?”

The Balance explains the bill well,

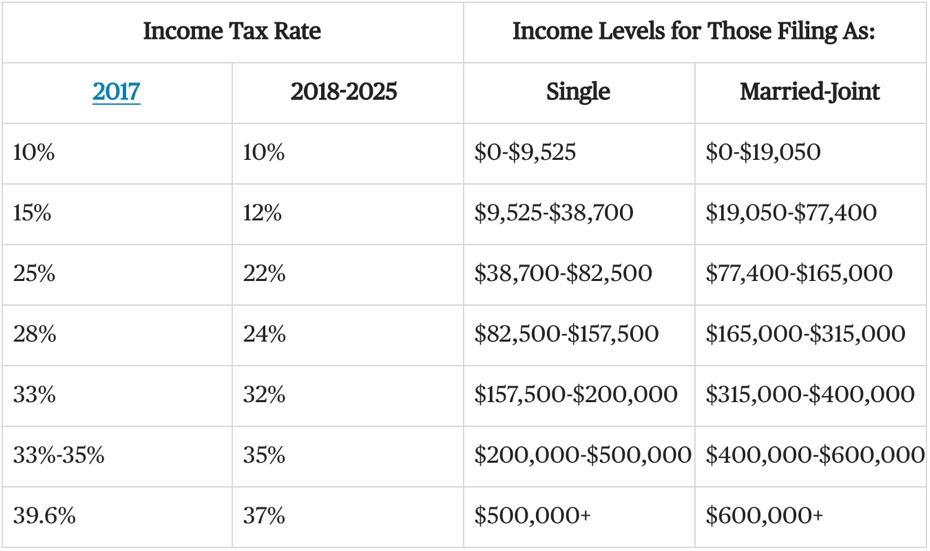

“The Act keeps the seven income tax brackets but lowers tax rates. Employees will see changes reflected in their withholding in their February 2018 paychecks. These rates revert to the 2017 rates in 2026.

The Act creates the following chart. The income levels will rise each year with inflation. But they will rise more slowly than in the past because the Act uses the chained consumer pride index. Over time, that will move more people into higher tax brackets.”

The article goes on to explain,

“The Act lowers the maximum corporate tax rate from 35 percent to 21 percent, the lowest since 1939. The United States has one of the highest rates in the world. But most corporations don’t pay the top rate. On average, the effective rate is 18 percent.”

Hopefully this helps you get a sense of how you’ll directly be affected. Please feel free to contact us if you’d like to further discuss the bill and how it specifically affects you.

Save Now, Then Save Some More!

We all know that saving for retirement is important, and it’s never too early to start. However, it never feels as simple as putting money aside – there’s always something that gets in the way. Whether it’s loans or debt that’s holding you back, is it better to pay off what you owe first or prioritize saving for your retirement account?

The Million Dollar Question

Building your retirement savings account is critical, but at what cost? Most of us enter the working world with some level of student loan, not to mention the possibility of developing more down the road – car loans, credit card debt, etc. – yet we’re being told to start saving for our retirement as soon as possible.

So how do you balance paying off owed money and simultaneously save for the future?

The Balance

As a financial advisor, I’m a strong advocate for saving for retirement as much as you can as fast as you can. That being said, I firmly believe the priority is to pay off your debt first, particularly the ones with high interest rate.

If you have high interest debt, then the amount you’re losing in interest each month may be more than what you could be earning in compound interest in savings.

I often tell my clients that once they’ve paid off high interest rate debt, then they can start contributing to their retirement savings account. This, of course, will look different case by case, but never rule out saving for retirement just because you owe money! Prioritize paying off your debt now as a way of being proactive about your future. The better you plan, the better you retire – and therein lies the balance.

Don’t Take My Word for It

Forbes weighed in on this topic as well,

“While this question is best put to a financial planner who can look at your entire financial picture, one way to think of it is that, if your student loan interest rate is 6.8%, the payments you make toward those loans give you a guaranteed 6.8% return on your money. Your retirement investments, especially after accounting for inflation, may not do as well. On the other hand, if you’re 50 and are behind on saving for retirement, you’ll still want to get the ball rolling since time is the biggest factor in how much your investments can grow. Bera says that for any debts with interest rates above 6%, she favors paying down debt over saving for retirement, but once you eliminate all those and are left with debts with lower interest rates, the emphasis would swing back to retirement.”

Low interest debt that’s tax deductible, like a mortgage, doesn’t need to be paid off before saving for retirement. However; I recommend you pay off all other high interest debt first, and then you can begin contributing the maximum to your retirement savings account.

If you’d like personalized advice on how much you should be paying/saving, one of our advisors will be happy to sit down with you and strategize how to get you on track for your best retirement.

Please schedule a call with us here if you would like to discuss your options.

Big News from the IRS

After two years without any changes, the IRS announced they will be increasing the 401(k) contribution limits for 2018. This is exciting news!

The increase in cost of living will allow individuals to contribute up to $18,500 ($500 increase) per year to their 401(k) retirement plan. Additionally, this increase will apply to other retirement accounts including 403(b) plans, most 457 plans, and Thrift Savings Plans (TSPs), however; the IRA and Roth IRA account contribution limits will not change. All employees should expect to see notifications from their employers about this increase.

Will This Really Make a Difference in the Long Run?

I always tell my clients that in order to grow their retirement savings significantly, they need to contribute as much as possible as young as possible. While an additional $500 per year may not sound like a major increase, ultimately these contributions will add up to a lot come retirement.

CNBC notes the significant difference of increasing your contribution to $500 each year, rather than simply putting an additional $500 in your savings account,

“As personal finance site NerdWallet points out, it could mean up to $70,000 more in your retirement account. The site calculated how much bigger your retirement fund would get if you started investing an additional $500 a year. It assumed a retirement age of 67 and a 6 percent annual rate of return. To give you an idea of just how powerful compound interest is, NerdWallet also highlighted how much money you’d have if you didn’t invest the $500 a year and simply kept it as cash:

- If a 30-year-old starts investing an extra $500 a year, it could mean an extra $70,212 in retirement, versus $18,500 saved in cash.

- If a 40-year-old starts investing an extra $500 a year, it could mean an extra $34,712 in retirement, versus $13,500 in cash.

- If a 50-year-old starts investing an extra $500 a year, it could mean an extra $15,202 in retirement, versus $8,500 in cash.”

How the Increase Positively Impacts Your Taxes

In addition to increasing your retirement savings, your taxable income will also be reduced when you contribute the additional $500.

If you have an employee contribution matching plan, a good rule of thumb is to contribute the maximum matching amount so you take full advantage and not leave any money on the table. However, if you can contribute more and maximize your 401(k) contributions each year (coupled with compounding interest), you’ll have a much larger retirement savings account.

Schedule a free call with us today if you have any questions regarding the increase in 401(k) contribution limits for 2018.

When you retire there are two important things that you want to know you have covered – a healthy retirement account with adequate money to support you throughout your retirement years, and medical/health coverage that will protect you throughout the years of aging that can often bring on increased medical expenses.

Fortunately, for federal employees, your federal retirement savings and FEHB (Federal Employee Health Benefits) coupled with Medicare work together to provide those two things. The United States Office of Personnel Management elaborates on the important role of the FEHB, “The FEHB Program can help you and your family meet your health care needs. Federal employees, retirees and their survivors enjoy the widest selection of health plans in the country. You can choose from among Consumer-Driven and High Deductible plans that offer catastrophic risk protection with higher deductibles, health savings/reimbursable accounts and lower premiums, or Fee-for-Service (FFS) plans, and their Preferred Provider Organizations (PPO), or Health Maintenance Organizations (HMO) if you live (or sometimes if you work) within the area serviced by the plan.” FEHB and Medicare work well together to provide a more comprehensive coverage and fill any gaps that may exist. When you retire, Medicare will be you and your spouse’s primary health insurance coverage and your FEHB will be secondary coverage. So, if Medicare covers 80 percent of a bill, FEHB will then kick in and most likely cover the other 20%. However, if you are a federal employee that continues to work beyond the age of 65, FEHB will remain your primary coverage and Medicare your secondary until you retire.

Medicare provides health insurance coverage for people that are age 65 or older (or for some with disabilities that are under the age of 65). Original Medicare has two parts: Part A & Part B which provide hospital insurance and medical insurance. There is also Medicare Advantage which has parts C & D and offers those enrolled private sector Health Maintenance Organizations (HMOs) or Preferred Provider Organizations (PPOs) coverage. Because federal employees have both Medicare and FEHB, they typically enrolled in Original Medicare. Medicare Part A has no premium associated with it and covers hospitalization so most people will choose to enroll in it. Medicare Part B does have a monthly premium and determining whether or not you need Medicare Part B is a more difficult decision that may be best discussed with your physician and your federal retirement planner. Ultimately, deciding what is best for your retirement is a personal decision and one that should be discussed with your federal retirement planner but it is important to note that you should never cancel your FEHB, regardless of what you decide. If you want to explore using Medicare instead of your FEHB, simply suspend it for a period of time so that, should you choose to, you can reactivate it at a later date. If you completely cancel your FEHB you cannot get it back at a later date.

Retirement planning is one of the most important ways to provide you and your family a safe and secure financial future. It can be difficult to anticipate just how much you will need for retirement because of things like inflation, cost of housing, preparing for things like potential health problems that could arise, etc. The sooner you start saving for your retirement, the better. Because of this, the sooner you contact an experienced federal retirement planner, the better. A federal retirement planner will be able to assist you in anticipating future needs and saving enough money for a good retirement.

Many people put off retirement planning assuming they have time to figure it out, particularly if they are young and other expenses seem more pressing. It is never too soon to start saving for retirement because the decisions you make now with your money will dramatically impact your retirement savings. CNBC explains just how important making smart decisions with your money now is and how it will impact your retirement savings in the future, “This is amply demonstrated by a 2012 survey of retirees by Bankers Life and Casualty’s Center for a Secure Retirement. When asked to give younger people just one piece of advice, 39 percent of survey participants said “Save for the future”…And when asked about the most important piece of financial advice they’d give, 93 percent of those retirees said start saving early, and 84 percent urged younger people to contribute to their workplace retirement plan…Here’s an illustration showing why that’s true: Suppose you’re 30 years old and for the next 35 years you contribute $5,000 a year (well below the maximum), earning 8 percent per year. At age 65 your account will be worth $861,584. But if you delay your participation just one year, starting instead at age 31, your account will be $68,451 less! If you contribute $1,000 a month and wait a year to start, your loss will be more than a quarter of a million dollars!”

Armed with retirement saving goals you can make choices now about how you spend your money. If you go out to frequent, expensive dinners with your spouse and consider eliminating 1 or 2 of those dinners per months you could be able to contribute an additional $100 – $200 dollars which translates to an additional savings of $1,200 – $2,400 per year which then compounds over time to dramatically increase your retirement savings down the road. Small changes with how you spend your money now can mean the difference between a retirement spent scrimping and saving and a comfortable retirement spent relaxing, traveling, and enjoying life.

When it comes to federal benefits there are a lot of acronyms and it can be a little confusing to understand what each one means and how it impacts your benefits. One such acronym is FEGLI which stands for Federal Employees’ Group Life Insurance. It is important for any adult to consider life insurance because you cannot anticipate the unexpected and you do not want to leave your spouse or family stranded without a safety net.

Federal life insurance is unique and a bit confusing which means that many federal employees have no idea how their life insurance actually works. With FEGLI, the government pays a portion of the cost of your life insurance. Every eligible federal employee is automatically enrolled in FEGLI’s basic insurance program unless you waive your coverage. Your coverage is based on your annual income which is then rounded to the nearest $1,000 and then added to that is $2,000 which is called the BIA or Basic Insurance Amount. The government pays 1/3 of the total cost of your federal life insurance. Generally speaking, FEGLI functions similarly to non-federal life insurance but there is one difference, as noted by the United States Office of Personnel Management, “Unlike many other employer-sponsored life insurance programs, FEGLI coverage can be continued into retirement. The FEGLI retirement benefit is prefunded by premium costs so that after age 65 (or at retirement, if later) some coverage can be continued by retirees at no cost. The net effect of the level premium and post-65 benefit is that younger enrollees’ premiums cover the cost of coverage they currently have, and also pre-funds a portion of the costs related to coverage they will have later in their careers and in retirement. Since the government contributes a share of the Basic premium, the employee share remains relatively competitive with the cost of private term insurance.”

There are 3 types of options insurance if you choose to enroll in optional insurance: Option A-Standard, Option B-Additional, and Option C-Family. It is challenging for anyone to determine how much life insurance they need. Fortunately, if you work with an experienced federal retirement planner they can assist you in calculating your FEGLI needs. Life insurance needs calculator can be found on www.lifehappens.org.

Call to our office at any time

Our support team

16430 N Scottsdale Rd Suite

150 Scottsdale, AZ 85254

8:00a - 4:30p

Monday to Friday