This rollercoaster of a year is rapidly drawing to a close, and that means it’s time to adjust your financial plan for 2021. If you haven’t thought about your retirement savings for a while, that’s okay — you’ve probably had a lot of other things on your mind! But before the New Year arrives, you’ll want to look over your Thrift Savings Plan (TSP) contributions and make some adjustments.

An annual review of your retirement savings and financial plan is always a good idea, but this year it’s even more important. That’s because there are big changes to TSP rules about catch-up contributions coming your way. But unlike most of the surprises that popped up in 2020, this is news that should actually make your life easier.

Here’s what you need to know.

Catch-up Contribution Basics

First, a definition. Federal employees who contribute to TSP accounts for retirement are subject to certain rules about how much money they can invest. IRS rules limit you to $19,500 per year — if you’re under age 50. But once you turn 50, you are allowed to contribute more. Catch-up contributions refer to the allowable amount over the $19,500 limit that you can contribute to your TSP between age 50 and the date of your retirement.

Catch-up contributions are designed to help people who are nearing retirement age pad their TSP accounts so they can reach their goals. Once you turn 50, there’s not as much time for compound interest to accrue and grow your nest egg, but adding more cash will help you build a solid foundation for future income. They’re called catch-up contributions in recognition of the fact that many people didn’t immediately open a retirement account when they enlisted or got their first job. Whether you waited a decade to open your TSP or just weren’t able to max out your contributions when you were younger, catch-up contributions give you a chance to make up for lost time now, while you are earning more at this stage in your career.

Catch-up contributions allow you to invest an additional $6,500 per year in your TSP once you turn 50. That brings your total allowable contributions for the year to $26,000 — a big boost to your savings if you can take advantage.

Rule Changes for 2021

If you are over 50 and already taking advantage of catch-up contributions, you know that the old rules were a bit challenging. Up until now — and through the end of 2020 — anyone wishing to make catch-up contributions had to fill out two different forms with your employer: one for your regular contributions of up to $19,500 each year, and a separate form for the catch-up contributions of up to $6,500 each year. This system also required double the paperwork for HR reps, making the process ripe for errors.

The biggest potential problem? Making a mistake along the way that could shut you out of your 5% match, leaving you with less retirement savings than you would normally be entitled to.

Given the issues with the old system, the 2021 catch-up contribution rule change is good news.

Instead of the extra paperwork and separate contributions, the new rules employ what’s known as the spillover method to calculate catch-up contributions. This means that you only need to fill out one form to elect to make TSP contributions. You’ll simply let your employer know how much of your pay to sweep into your TSP account, and that’s it.

On your employer’s end, they’ll figure out at what point your contributions are in excess of the $19,500 and “spill over” into catch-up contributions. This is now automatic, and you’ll never have to think about it once you decide how much to contribute and file your form.

And honestly, this is how it should be.

Your Action Plan for Catch-up Contributions

Now that making catch-up contributions is easier than ever before, it’s time to take advantage! Here’s what you need to do:

Step One: Review Your Contributions

How much are you contributing to your TSP right now? If you were hired (or rehired) starting October 1, 2020, you were automatically enrolled at 5% of your salary — the exact amount you need to max out your matching funds from your employer.

If you were hired before then, take a look at your last pay stub to see how much you’re contributing. If it’s not at least 5%, you definitely want to increase your contribution to reach that amount — anything less, and you’re leaving free match money on the table.

Step Two: Challenge Yourself to Max Out

Even if you’re already contributing 5% of your salary to your TSP, you can still do more. Remember, the limit for workers under age 50 is $19,500 per year ($750 per biweekly paycheck). If you’re over 50 and adding catch-up contributions, the limit is $26,000 ($1,000 per biweekly paycheck). If you’re not hitting that mark and want to, ask yourself how you can make room in your budget to get a little closer.

If you’re like most people, 2020 probably saw a decrease in some of your spending, particularly on things like travel, eating out, movies, sporting events, and the like. If you normally spent $100 per month on these activities, consider increasing your contributions by that same $100 — you probably won’t miss it.

If you received a step increase or promotion, you can also try putting most or even all of your income boost into your TSP. Because this money comes out of your check before you even cash it, retirement contributions can be “invisible.” You won’t notice that a little extra has come out of your check — until you look at your TSP balance, that is!

Step Three: File the Paperwork

Once you’ve decided on your new contribution amount, it’s time to file the paperwork. The new system begins on January 1, 2021, so ideally you will complete your forms in time to start the New Year right.

Most civilian agencies have electronic payroll systems, so use yours to increase your contributions online. Armed forces members can use myPay (Air Force, Army, Marine Corps, and Navy) or Direct Access (Coast Guard and NOAA Corps). USPHS Commissioned Corps members, however, need to fill out paper forms instead, so contact your payroll officers for more information.

Remember, your goal is always to contribute as much as you possibly can to your TSP. The minimum should be 5% so as to get the full benefit of your matching funds, but that’s just for starters. Challenge yourself to do more in 2021 — including taking advantage of catch-up contributions if you’re over age 50.

For the first time in over 15 years the Thrift Savings Plan is coming out with a new lineup. To give you a quick recap the S and I fund were introduced to the TSP in 2001 and our first, now retired, Lifecycle fund L 2010 in 2005.

With L 2020 moving into retirement today and new five-year increment Lifecycle funds being available its a good time to learn and review your fund options.

As you may already know, each L Fund is made up entirely of the five core funds, G, F,C,S and I in different allocations. These target date funds automatically adjust to more stable funds as you get closer to the time you plan to retire.

The new lineup consists of L Income, L 2025, L 2030, L 2035, L 2040, L 2045, L 2050, L 2055, L 2060 and lastly L 2065.

If you have questions on your TSP allocations or if these new Lifecycle funds are right for you please get in touch.

Losing a loved one is always difficult, and the death of a parent can be particularly unsettling. Many people describe the loss of their parents as being orphaned: No matter how old you are or how well established in your life, this major loss will lead you to reevaluate your place in the world.

In addition to strong feelings of grief, losing a parent also means dealing with a mountain of paperwork. As an heir to their estate, you’ll be left to sort out their finances, put their affairs in order, and complete any final wishes about the things they’ve left behind.

From requesting death certificates to preparing a final tax return, there’s a lot to keep track of — it’s completely natural to feel overwhelmed. To help you sort through all the paperwork and keep things organized, we’ve put together this checklist to walk you through the major steps of handling your parent’s finances.

Get Copies of the Will

It’s best to have the will as early as possible, especially if there are instructions about funeral arrangements included in it. This will help you planning your parent’s final resting place and will be necessary for appropriately dividing the estate among heirs in the coming weeks and months.

Gather Identifying Documents

As you deal with various financial entities, you’ll need to prove your parent’s identity. To do this, you will need:

- Birth certificates (for your parent and their children)

- Social Security cards

- Marriage certificates

- Divorce paperwork

- Military discharge papers

You may need some or all of these identifying documents for your other deceased parent and any of your parent’s heirs as well.

Get Copies of the Death Certificate

Most people are surprised at how many copies they will need of the death certificate to send to various financial institutions. Many experts recommend ordering up to 20 copies so you’ll have what you need and avoid the hassle of having to order more. You can usually order these from the funeral director or from your local Board of Health.

Inform Your Parent’s Employer

If your parent was still working, contact human resources to inform them of their death. Ask for information about benefits, which may include additional life insurance, health insurance, and retirement plan information.

Inform the Social Security Office

If your parent received Social Security, you’ll need to call to let them know your parent has died. They can help you switch payments to a surviving spouse if necessary and let you know if you or anyone else is eligible for a death benefit.

Inform the Veteran’s Administration

If your parent was a veteran, the VA may offer special funeral arrangements and other benefits, including survivor benefits.

Start the Probate Process

Having your parent’s will is only the first step to dividing their estate. Though a surviving spouse will typically get everything upon the death of one parent, when both are gone, you’ll have to go through probate court to authenticate the will and officially divide the estate’s assets. Each state has different rules and regulations, so working with a lawyer is a good idea.

Tip: If you are named the executor of the estate in the will, keep receipts for your related expenses so you can be reimbursed from the estate.

Settle a Living Trust

If your parent created a living trust instead of a will, you will be able to avoid probate court to divide the assets. Instead, the designated trustee (which could be you, a relative, or a third party) will settle the estate. This involves gathering all the trust’s assets, paying off any bills or debts, and dividing what’s left among the named beneficiaries of the trust.

Gather Financial Paperwork

To resolve your parent’s finances—whether they had a will or a trust—you’ll need information on all their accounts. These may include:

- Bank accounts, such as checking and savings accounts

- IRAs

- Pension account information

- 401(k) or 403(b) retirement plans

- Annuities

- Brokerage investment accounts

- Life insurance policies

- Deeds for other property and assets, such

You’ll also need to gather information about accounts to which they owe money. These may include:

- Tax returns

- Mortgage statements

- Other loans, including student loans, home equity lines of credit, car loans, etc.

- Utility bills for items like cable, electricity, gas or fuel oil, etc.

- Credit card statements

Tip: If you aren’t sure that you know about all of your parent’s accounts, check their mail for the next three to six months to intercept bills and paperwork. You may find it easier to have their mail forwarded to you for convenience.

File a Final Tax Return With the IRS

You will need to file a final tax return for your deceased parent. Keep all of the paperwork you’ve gathered handy for filling that next April, and be on the lookout for W-2 forms and any final tax documents as they become available in January so you can file accurately.

Make Necessary Cancellations

Use the paperwork you’ve gathered as a guide to help you cancel accounts that are no longer necessary. These may include:

- Credit cards

- Lines of credit

- Health insurance

- Auto insurance

- Voter registration

- Memberships to clubs, subscriptions, etc.

- Driver’s license

- Email, social media, and other online accounts

Change or Close Accounts

If you have a surviving parent, you may need to transfer utility bills, mortgage accounts, and other property, assets and bills into their name. Review the financial documents to determine which payments still need to be made and arrange for them to be paid without interruption.

If you do not have a surviving parent, learn how to close accounts that are no longer needed and how to set up payment for debts that must be cleared.

File Claims for Benefits

You’ll need to file a claim to receive life insurance benefits if your parent had a policy. Likewise, you may be eligible for benefits from their retirement accounts, depending on their designated beneficiaries. A professional financial planner can help you file these claims and make the most of these benefits.

Get Professional Help

Depending on the complexity of your parent’s finances, dealing with their final affairs can be a major challenge. A good probate lawyer and knowledgeable financial planner will help you sort through the details and ensure that you don’t miss anything as you complete this process. They will also advocate for you as you work through this difficult process.

If you need help getting your own finances in order, we can help. Reach out any time for advice on how to handle your finances and plan your estate — a gift of peace of mind for yourself and your future heirs in their time of need.

There’s never been a better time to make sure your finances are in order.

It’s stating the obvious, but we are now all living through a period in history none of us will ever forget — “uncertain times,” indeed. The impact on our families, communities, and the country as whole has been, and will continue to be, profound. It’s a scary time, but there’s one important piece of advice that can see you through the worst:

Focus on the things you can control.

As the old saying goes, “When life gives you lemons, make lemonade.” Today’s economy is a real lemon, but obsessively watching the news and the state of the stock market isn’t going to help. Instead, take a look at what you do have and make the absolute most of it. In this way, you’ll be squeezing maximum value out of your personal finances and positioning yourself for a better tomorrow.

Here is a checklist of action items that you can fine-tune before life speeds back up again. If you’ve never thought about some of these points, that’s okay. Now is the perfect time to get started.

Estate Planning

Most people do this once and forget about it for decades, but your estate planning needs change just as you grow and change over the years. Make sure your current plans still meet your needs.

- Review Your Beneficiaries. This includes your investment accounts, retirement accounts, Thrift Savings Plan (TSP), last paycheck, FERS lump sum benefit, bank accounts, and life insurance both private and Federal Employee Group Life Insurance (FEGLI). Make sure your beneficiary choice and contact information is up to date.

- Review Your Documents. This includes your Last Will and Testament, Power of Attorney, Living Will and perhaps a Living Trust. Are they up to date? If you need to get started on any of these, we can provide resources for you.

- Inform Your Loved Ones. Should something happen to you, do your loved ones know what to do? Where to find your documents? Who to contact? Create a document and provide both digital and hard copies of this important information.

Insurance

If your insurance auto-renews each year, you might not have the correct coverage for your current needs. You also might be overpaying!

- Review Your Coverage. Is your homeowners insurance sufficient? Should you still be carrying collision coverage on an older vehicle? Do you have enough cash on hand to raise your deductible and enjoy premium savings? Ask for new quotes to see how these changes affect your bottom line. This is also a great time to ask for discounts.

- Record Your Belongings. Take pictures or video of your valuables to provide to the insurance company if they are stolen or destroyed. It’s the best way to streamline a claim and make sure you get what you’re entitled to.

- Consider an Umbrella Policy. This extra liability insurance is typically a great value when it comes to protecting yourself from a lawsuit that could ruin you.

- Recalculate Your Life Insurance Needs. Do you have the right amount of life insurance to protect your family? Try a simple calculator to see how much you need, or get in touch for help. FEGLI has some good options but some become expensive as you age.

Budgeting

When’s the last time you reviewed your monthly budget? Of course, you don’t want to use the last 30 days of spending as a guide, since many normal spending habits have been forced to change as we practice social distancing.

- Use 2019 Numbers. This will help you get a more accurate view of your typical income and spending. By looking at real numbers, you can see how much you actually spend in different categories and make some adjustments if needed.

- Review Your Auto-Pay Expenses. It’s so easy to forget about old subscriptions and services we no longer need — but that we still pay for via auto deduction. Cancel these budget vampires and breathe a sigh of relief.

Taxes

Recent tax law and IRS rule changes mean that you might be missing out on some savings.

- Consider Converting to a Roth IRA. With many IRAs being down in value, converting a Traditional IRA to a tax-free growth Roth IRA may save money on taxes. We’re happy to discuss your options to help you make the most of your retirement.

- Set Up IRA Contributions: See if you can increase your contributions to maximize your savings. If you didn’t make 2019 IRA contributions, you can still do so until July 15, thanks to a COVID-related IRS extension. And the TSP allows for contributions of $19,500 plus a catch-up contribution of $6,500 for those aged 50 and older.

- Explore Charitable Giving: The CARES Act has expanded deductions for charitable giving this year, so it’s a great time to help worthy organizations. Qualified Charitable Contributions (QCDs) can help you to support causes you believe in using required minimum distributions from retirement accounts.

General Maintenance

With extra time on your hands, it also makes sense to do some general financial housekeeping to make it easier to review your paperwork in the future.

- Update Your Financial Dashboard. If you’re using personal finance software, be sure you’re linked to all your current accounts for accurate tracking and budgeting.

- Trash Old Documents. Be sure to shred those papers to protect sensitive personal information and account numbers.

- Organize Your Financial Files. Get those tax returns, insurance policies, and more into neatly labeled folders for ease of use later.

- Scan and Save Important Documents. If you don’t already have digital versions of your paperwork, take the time to scan them and create a digital filing cabinet now.

Some thoughts about planning for the future.

With your financial life organized and streamlined, you should feel much better about things. You have all of your information at your fingertips, and that makes it easier than ever to make some smart choices about the future.

If you’d like to talk about your investment options and financial planning needs, we’re always here to help. We know it’s a stressful time, and we pledge to do our best to provide clarity, transparency, and advice that will help you make your best moves in these difficult times.

Please reach out if you’d like more help with financial and retirement planning — we’ll be standing by!

In the meantime, stay healthy, safe and sane — and try to enjoy the lemonade you’ve worked to create out of this situation.

For those that served in the military, we thank you for your service. If you decided to move into civilian service after serving you have most likely heard about the opportunity to “buy back” your military time. According to OPM, “As a general rule, military service in the Armed Forces of the United States is creditable for retirement purposes if it was active service terminated under honorable conditions, and performed prior to your separation from civilian service for retirement.”

Although you may have heard about buying back military time the details and benefits may be a little unclear. So here is a brief explanation as to why you should consider acting soon to buy back your military time.

The FERS Annuity calculation is relatively straightforward. For every your of creditable service you get 1% (this varies for age 62 with 20 years and Special Provision) towards your retirement annuity calculation. That percentage is then applied to your High-3 Salary.

Assuming a $100,000 high-3, 28 years of service will generate a gross annuity of $28,000 / yr.

$100,000 x 1% x 28 = $28,000 / yr

How much does it cost?

If you want your military time to count toward a FERS annuity, then you need to make a Military Service Credit Deposit to buy into the annuity. First, you will need to get your pay info for each year of your military service. If you can’t locate that info you can request it from your branch of the military with your DD-214. Your Military Service Credit Deposit amount is based on a percentage of your pay as shown in the table below. Keep in mind, there is only a two year grace period to make the deposit before interest begins to accrue.

Service Deposit Due

Through 12/31/98 3% of military basic pay

1/1/99 – 12/31/99 3.25% of military basic pay

1/1/00 – 12/31/00 3.4% of military basic pay

1/1/01 to present 3% of military basic pay

Who should buy back their military time?

I can’t say everyone should as I’m sure there are a few rare cases where it may not make sense. However, after consulting with thousands of federal employees about retirement I have yet to come across one veteran that would not benefit greatly from buying back their military time.

How long does it take to breakeven?

This is the big question. How long will it take me to make back what I have to pay to buy back my years of service? Again, everyone’s scenario is different but here is an example showing a breakeven calculation. You can run the same calculation using your info and I think you’ll find that it doesn’t take long for you to recoup the cost to buy back your years.

Breakeven Calculation Example:

Military Time: 8 years 6 months

Deposit without Interest: $3,200

Interest: $2,500

Deposit including interest: $5,700

Breakeven Calculation

8.5 years x 1% = 8.5%

8.5% x High 3 $100,000 = $8,500

$8,500 Increase in Annual FERS Annuity

$5,700 / $8,500 = 0.67 Years

8 Months to Breakeven

In the example given, the cost of buying back military time would be recouped in just 8 months!

The Cost of Not Buying Back Military Time, Over Time – excluding COLA

(using the example given)

10 Years: $85,000

15 Years: $127,500

20 Years: $170,000

25 Years: $212,500

30 Years: $255,000

Of course, depending on your deposit, interest and current salary your breakeven will be different. If you have waited several years, your interest portion could be more than the original deposit owed, but don’t let that be discouraged. In most cases buying back military time will make financial sense and have a breakeven of just a few years or less.

Survivor Benefit

Additionally, if you elect a survivor annuity for your spouse buying back military time will increase their lifetime survivor annuity.

Added Bonus

Everyone has a different situation, however there is an added benefit to buying back military service time. It may allow you to reach retirement eligibility earlier. For example, Mary is 60 with 17 years of civilian service and wants to retire, however she would need 20 years to do so without penalty. If she happened to be a veteran she could make a military credit service deposit to buy those years back and if those years put her over 20 years of total creditable she can retire on an unreduced annuity at age 60.

Next Steps

If you’re ready to take the next steps to buy back your military time to increase your lifetime payments from your FERS annuity you will want to begin by completing an Estimated Earnings During Military Service request form, RI 20-97. Be sure to include your Certificate of Release or Discharge from Active Duty, DD 214 then submit it to your branches military finance center.

Want to discuss how much more your FERS annuity will be as a result of buying back your military time schedule a quick 15 minute call with an advisor or visit Federal Retirement Services.

For participants in the Thrift Savings Plan (TSP), it’s more important to focus on tried-and-true disciplines that have worked over time versus what the stock market is currently doing or what the talking heads predict the market will do. Rebalancing is one such discipline that can potentially reduce risk and increase long term performance, and may also help reduce some of the worry that accompanies times of increased market volatility.

What is Rebalancing?

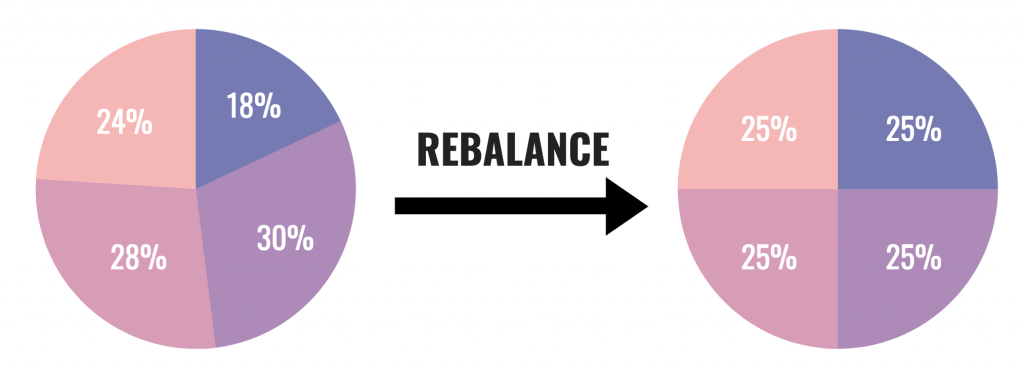

Rebalancing is the process of realigning the weightings of a portfolio to get back to a target asset allocation. It involves periodically buying assets that have decreased in value and selling assets that have increased in value. This discipline is intended to cause investors to buy low and sell high with the goal of maintaining an original desired level of asset allocation.

The figure below shows a target allocation with equal weighting into four different Asset Classes. If any one asset class moves above or below a predetermined percentage (ex. 3%, 5%, 10%) of its target allocations, it’s time to rebalance.

It’s Counterintuitive to Buy Low and Sell High

In times of market uncertainty and poor investment performance, selling better performing assets and buying more underperforming assets in your portfolio may seem counterintuitive. However, market corrections and deep bear markets represent rebalancing opportunities to increase ownership into positions that have experienced a significant drop in price. For example, if you were happy to buy the C Fund at a particular price but then the price drops 15%, 20% or more, your first instinct might be to stop the bleeding and sell. However, if you do that you’ve now locked in your loss. Setting up rules for when to rebalance before the market declines may save you from making the typical investor mistake of buying high and selling low.

When to Rebalance?

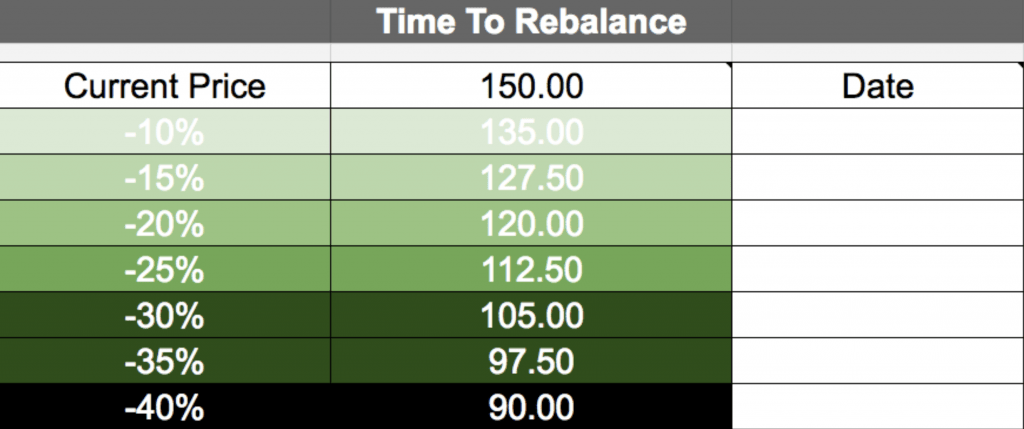

There is no “perfect” time to rebalance. If you want to take a disciplined approach that removes emotion, consider rebalancing every time your TSP drops or increases in increments of 3%, 5% or 10% in value. The percentage you select isn’t as important as committing to rebalancing when your reach the threshold. A variation of this method is to rebalance anytime one or more of the funds is 3% or greater outside of it’s target allocation. Alternatively, you can use one of the broad market indexes as an indicator of a good time to rebalance. Hypothetically if the S&P 500 drops 10%, you could use this as a time to buy low and sell high instead of panicking. Buy shares of investments when they are down so you will have more ownership if the investment recovers. Note: If you have your entire TSP balance in one fund or just in the C, S or I, rebalancing may not be as effective if all funds are similarly down.

The figure below shows an example of when to rebalance and take advantage while others may be panicking and making mistakes.

Simple and Actionable

Imagine how empowering it would be to have a simple, actionable plan in place if the stock market drops 10%, 15%, 20% or more that could actually help your investments long term. Consider letting your portfolio tell you when to take action and rebalance, not a media personality whose primary job may be to keep you afraid and tuned in for higher ratings.

Next Steps

- Establish the appropriate asset allocation for your personal risk tolerance and time horizon (when you need to use the money).

- Rebalance (buy low, sell high) your asset allocation established using one of the methods mentioned above.

- Update step one every few years.

Good luck!

Rebalancing is a strategy that can’t guarantee against a loss or better portfolio performance and could result from missing out on additional gains from appreciated assets. This is not intended to be financial advice. Please consult an investment professional on any strategy or your individual situation. Examples are for illustrative purposes only. Past Performance doesn’t guarantee future results.

Effective September 2019, there will be significant changes made to the Thrift Savings Plan (TSP). These changes will be focused on withdrawal options that have previously lacked flexibility causing many to look for alternative options that offer more accessibility and control to their retirement savings.

Here’s a breakdown of the upcoming changes being made to the TSP:

Multiple Age-Based Withdrawals:

- Currently: Participants only have the opportunity for one partial withdrawal in-service or post-separation.

- Upcoming Change: Multiple age-based (for those 59½ or older) in-service and post-separation partial withdrawals will be allowed. You won’t be able to take more than one every 30 days, and you’re limited to four age-based in-service withdrawals per calendar year.

Choice of Traditional or Roth or Both for Withdrawals:

- Currently: If you have both Traditional and a Roth balance, the only way to take a withdrawal is on a pro rata basis.

- Upcoming Change: You’ll be able to choose whether your withdrawal comes from your Roth balance, Traditional balance, or a proportional mix of both. You can still do pro rata basis; however, the additional option of selecting the mix is also available. This change applies to all types of withdrawals.

Required Minimum Distributions (RMDs):

- Currently: Full withdrawal election is required after you turn 70½ and are separated from federal service.

- Upcoming Change: You will no longer be required to make a full withdrawal election after you turn 70½ and are separated. You will still need to receive IRS-required minimum distributions (RMDs).

Installment Payments – Monthly, Quarterly or Annually:

- Currently: Only monthly installment payments are available and you can only change the amount of your payment once during open season (October 1 and December 15).

- Upcoming Change: If you’re a separated participant, in addition to the option of monthly payments, you’ll be able to choose quarterly or annual payments, and you’ll be able to stop, start, or make changes to your installment payments at any time.

What’s Still Lacking?

In my opinion, the TSP still has room to improve the installment payments. A few small changes to the ways federal employees can withdraw their income could potentially help TSPs last longer in retirement.

Here are a three ways the TSP can still improve installment payments.

Monthly Payment Flexibility

Allowing participants to decide which of the TSP Funds are used/sold to generate monthly installment payments would have a significant benefit. As an example, let’s say a retired participant has their TSP allocation set to 50% C Fund and 50% F Fund and they are taking monthly payments of $1,000 each month. The TSP will sell the needed amount of shares to generate $500 from the C fund and $500 from the F Fund. The C Fund tracks the performance of the S&P 500 Index, which can experience shape price fluctuations and cause the participant to sell a variable amount of shares from month to month based on the C Fund performance. If the C Fund is down 15%-20% or more, the participant would have to sell considerably more shares to generate their monthly income. This is referred to as reverse dollar cost averaging and poor returns early in one’s retirement can have serious long term effects.

Ability to Take Income from Dividends and Interest

In order to take monthly payments, you must sell shares. Many investors taking income from their retirement accounts prefer to spend only the dividends and interest generated by their investments. This is a concept that has been around for a long time, and for good reason. It works and does not put additional pressure on investments portfolios due to selling shares when the investments are down. This option may never be available in the TSP since most employer-sponsored retirement does not offer this level of flexibility.

Investment Options

There are no new funds added to the TSP. The five core funds remain plus the L Funds, which are a blend of the five core funds based on your proximity to retirement. For many years feds have called for additional investment options, but it doesn’t appear any new funds will be added in the near future.

In summary, the TSP Modernization Act is an improvement over the current rules; however, there are areas that further improvement can be made. The challenge is how to make continual improvements without increasing costs. When it comes to the question of whether or not to roll over your TSP to an IRA in retirement, here is an apples to apples comparison. Ultimately, you need to do your own due diligence and make the best decision that best suits your needs in retirement.

If you’d like to discuss your TSP options with us, book a call using this link and we’ll be in touch with you shortly.

There’s great comfort in knowing you can weather the most common “financial emergencies” like a new transmission for your car, a trip to the emergency room and even the dreaded AC unit replacement. It’s important to have an emergency fund in place, but what’s considered a viable amount and how long does it take to build? Can it be done in a year or less? The short answer is with some work, yes.

First Things, First

Before rolling back your sleeves and building an emergency fund, make sure you address any outstanding credit card balances first. Dave Ramsey suggests setting aside $1,000 into your savings first to give some breathing room, then paying off credit cards so you can start building your full emergency fund.

Another potential misstep would be calling your emergency fund a zero balance credit card or HELOC (Home Equity Line of Credit). Many folks use this approach because they don’t want their savings earning close to zero interest. I don’t recommend this for two reasons. First, the last thing you want to do (if faced with a financial emergency) is to add fuel to the fire by adding debt. Second, you shouldn’t be overly concerned with growth or how much interest you’re earning with money you may need to spend within 36 months. You just need to know the money will not lose value and be accessible.

Establish the Right Amount

The tried-and-true way to establish an emergency fund is having three to six months of spendable income in place. For example, if you are paid bi-weekly, take your direct deposit amount and multiply it by 6 (3 months) or 12 (6 months) and that’s the target number to have in your emergency fund. I recommend closer to 6 months for an added sense of security – better to have it and not need it than to need it and not have it.

Here are five practical ways to build your emergency fund within a year. They can be used individually or combined with each other to establish your emergency fund.

1. Set Up An Allotment from Your Paycheck

If you’re paid in a regular frequency (bi-weekly or monthly), this is a simple and effective way to reach your savings goal. For example, let’s say you want $9,000 in your emergency fund in one year. If you’re paid bi-weekly, you have 26 pay periods every year: $9,000 / 26 = $346 allotment every paycheck.

This strategy requires two disciplines. The first is to set up your emergency fund at a financial institution other than the one you have your primary checking account. This removes the temptation – out of sight, out of mind. The second is to not overdo it. This plan will backfire if you get too ambitious and set up an allotment for an amount that is not sustainable. If you can’t hit your twelve month goal, then adjust the timeframe or implement other strategies.

2. Sell Your Stuff

This one is pretty self-explanatory, but it’s also easier said than done. It’s a challenge to let go of stuff we never use – we get sentimental or rationalize unlikely scenarios where something may come in handy. A good rule of thumb is if you haven’t used it in the last year, you are not likely to use it again. Earn some extra cash and sell your stuff to someone who needs it more.

3. Reduce Retirement Account Contributions (401(k) / TSP / IRA / 403(b) / 457)

This one tends to raise some eyebrows and cause controversy, but temporarily reducing your 401(k) or other retirement account contributions for the sake of building your emergency fund may be the right approach. Once the money enters into your retirement account, there could be penalties for accessing the funds should you get into a financial pinch. If you have a company match, you may want to consider contributing the minimum amount to receive the match. Prioritize the emergency fund first.

4. Tighten Up Your Budget

If you honestly track your spending for 30 days, you will likely find one or two spends that cause you to be a little upset with yourself. Commonly eating out is one of the usual suspects. Amazon is also a frequent offender. Look over what you’re spending and adjust accordingly – it’s that simple. I like to see what percentage each category of spending represents (insurance: 8%, eating out: 5%, mortgage: 25%, etc.). Give it a try, the results may surprise you.

5. Get a Side Job

I realize this strategy may not initially get you excited, but keep in mind this is a temporary means to an end. The good news is there are so many opportunities today to pick up a side job with flexible hours. Rideshare companies like Lyft and Uber are just one of many ways to generate some extra income with flexible hours. Get creative, and have fun with it.

When you hit your emergency fund goal, you can go back to your retirement account funding – ideally 15% or more. Don’t forget all the lessons learned from reviewing your budget and spending. Keep the unnecessary spending down. Should an emergency occur and you have to tap into your savings, you want to be well-prepared to replenish your emergency fund. Good luck!

If you’d like to discuss your emergency fund options with us, book a call using this link and we’ll be in contact with you shortly.

Planning for retirement is a significant undertaking, especially for federal employees. The Federal Employee Retirement System (FERS) offers a robust benefits package which includes an annuity also know as a pension, which is generally considered the most important benefit for retirement income planning. If you’re in FERS, you can actually lock in a 10% increase to your retirement annuity for the rest of your life.

First let’s look at how to calculate the Regular FERS annuity.

Example 1:

Let’s assume this individual is 61 years old with 28 years of service and a high 3 average pay of $100,000.

High 3 x Years of Creditable Service x 1% = Annual FERS Annuity

$100,000 High-3, 28 Years of Service

$100,000 x 1.0% x 28 yrs = $28,000

28%

Total Basic Annuity: $28,000/year or $2,333/month

There’s also an enhanced formula that goes into effect for those who retire at 62 or older with 20 or more years of creditable service. This formula increases the multiplier from 1% to 1.1%. At a glance this appears to be a minor increase; however, it’s a 10% increase that will have a long term effect in your retirement income for the rest of your life. If you elect a survivor benefit, that will also be increased by 10% for your surviving spouse’s life.

Example 2:

Let’s look at another example, assuming the same person in the example above waited on additional year to age 62 to retire.

High 3 x Years of Creditable Service x 1.1% = Annual FERS Annuity

$100,000 High-3, 29 Years of Service

$100,000 x 1.1% x 29 yrs = $31,900

31.9%

Total Basic Annuity: $31,900/year or $2,658/month

This increase may or may not be a motivating factor for you, but when it comes to financial decisions that have long term implications, you’ll want to quantify what that decision means to you in terms of dollars.

Here’s a comparison of Example 1 versus Example 2 of the increase in the FERS annuity (not factoring in any taxes or other deductions) annually, monthly and cumulatively over 5, 10 and 20 years:

If you qualify for the 1.1% increase, run the same numbers then decide if it’s worth it to stay on the job or not. Also, keep in mind this is a simplified calculation. Other factors include: payment every year you work, 5% TSP match, workplace stress, your contribution to the TSP, COLA, possible increase in high 3, etc. Ultimately, you just want to get a general idea of what kind of money you’re walking away from should you decide to retire prior to qualifying for the 1.1% calculation.

If you’d like to discuss your options with a federal retirement advisor, book a call using this link and we’ll be in contact with you shortly.

Protecting our loved ones from financial burden and hardship is understandably a high priority for many folks. A lot of times this is accomplished through the use of life insurance. The key is to establish the appropriate amount of coverage to protect your family, then research the most cost effective way to provide that safety net.

The Federal Employee Group Life Insurance (FEGLI) Program offers four different options to choose from: Basic, Option A, Option B and Option C. The Basic coverage is the only option newly, eligible employees are automatically enrolled in unless they waive coverage. Alternatively, the remaining three coverages must be elected.

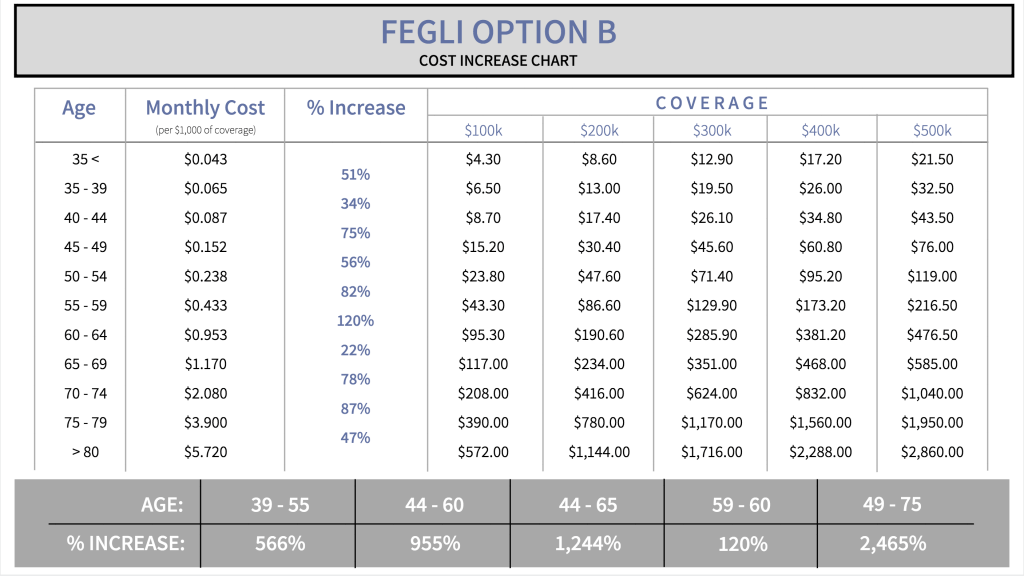

While Option B allows for the most coverage, it is also potentially the most costly option. Many people realize FEGLI Option B premiums do increase over time but they may not grasp the significance of the increase. For example, from age 44 to age 65 the premiums for FEGLI Option B increase by 1,244%.

The chart below shows the increase in FEGLI Option B premiums as well as how much you would pay on a monthly basis for various amounts of coverage:

So how do you avoid paying too much for your life insurance?

Establish the Right Amount of Coverage

Too often, people select an arbitrary figure for life insurance coverage ($250,000, $500,000, $750,000, etc.) without putting much thought into it. Maybe it’s just enough to pay off mortgages and other debts. However, the reality is that’s just the beginning of the assessment.

Take into consideration your family’s income needs, current investments, inflation, education needs (if you have children), survivor benefits from a pension and current in-force life insurance. Of course, you want to maintain the same lifestyle for your family, but you also don’t want to over-insure. Find the happy medium.

You can use an online tool to help you establish the appropriate amount.

With FEGLI Option B, you have the ability to select 1, 2, 3, 4 or 5 multiples of your salary rounded to the next $1,000. This means you have the opportunity to get as close as possible to your target coverage amount but it may be difficult to get the exact amount of coverage you need. The alternative is private level premium term life insurance where you can select the exact dollar amount of coverage.

Do Your Research

The biggest issue with FEGLI Option B is the extreme premium increases over time. The increase occurs every five years; more specifically, every time you have a birthday ending in 0 or 5. It’s hard to imagine, but the premiums increase over 2,400% from age 49 to 75 which means they become extremely high the older you get.

If you aren’t aware of these increases, you may inadvertently miss the opportunity to plan ahead and lock in lower rates with term coverage. In some cases, you may even receive a medical diagnosis causing you to be uninsurable. Essentially, you would be stuck paying high premiums and this could cause your household financial hardship in order to keep your family protected.

Good news is this is certainly something you can and should avoid.

The best way to avoid overpaying for life insurance is to do your research. Term life insurance offers the opportunity to lock in low-level premium payments that will last however many years you choose (15, 20, 25 or 30 year terms). Make sure you only shop A-rated insurance carriers and make yourself aware of any optional riders you can add to the policy – Accelerated Death Benefit / Critical Illness rider, Child rider, Spouse rider, Premium Waiver rider and Return of Premium ride, etc. You may opt to add one or more or you may find them unnecessary.

When it comes to getting life insurance, the sooner you get covered the better. If you have people that depend on you financially, start doing your research now and run a life insurance needs calculator. Typically, the entire process for getting private life insurance takes 30 to 60 days from application to approval, so it’s best to get a head start. I always recommend getting quotes from at least 3 to 4 different carriers, so you can compare your options and make sure you get fair pricing on your insurance coverage.

If you’d like to discuss your options with a federal retirement advisor, book a call using this link and we’ll be in contact with you shortly.

Call to our office at any time

Our support team

16430 N Scottsdale Rd Suite

110 Scottsdale, AZ 85254

8:00a - 4:30p

Monday to Friday